Is Mastercard a good business to invest?

5/8/20248 min read

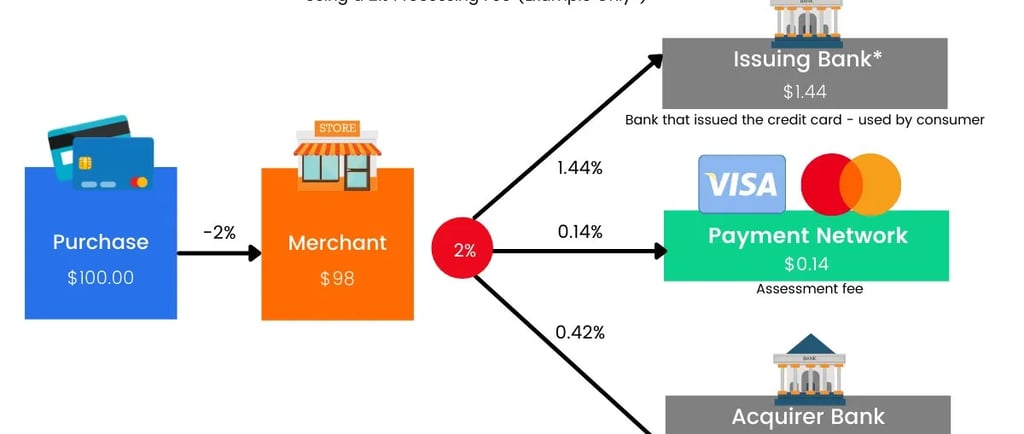

If you live in first world countries, it is almost certain that you would own at lease one Mastercard or Visa debit or credit card. Mastercard and Visa is neither a bank nor credit card company, instead, they partner with banks and finical institutions that issue the cards to consumers.

When you purchase something using Mastercard or Visa, the Mastercard or Visa charge a small fee to the merchant for processing this transaction. In simple terms, banks and financial institutions pay fees to Mastercard or Visa to its payment network.

Fig.1 Simple illustration of interaction when making a purchase (Source: finchat,io)

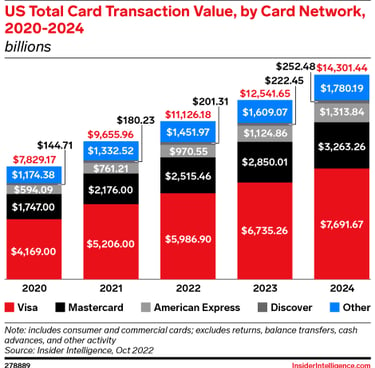

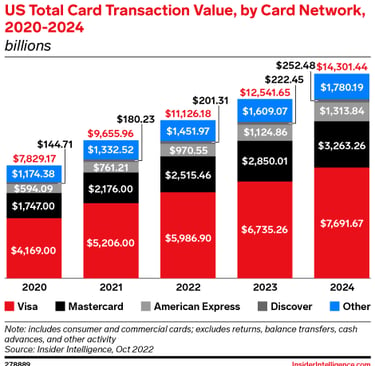

US card network transaction value is expected to surpass $14 trillion in 2024 (per Insider Intelligence), with payments behemoth Visa accounting for 57.3% of the business and followed by Mastercard.

Fig.2 US total card transaction value

How Mastercard (MA) make money?

Mastercard makes money through several key revenue streams, primarily centered around its payment network and value-added services. Here’s a detailed breakdown:

Fig.3 How Mastercard make money

1. Transaction Processing Fees

Mastercard earns fees from processing payment transactions. This includes:

Authorization: Verifying the availability of funds.

Clearing: Transmitting transaction details between the acquiring and issuing banks.

Settlement: Transferring funds between banks.

2. Assessment Fees

These are fees charged to issuers and acquirers based on the volume of activity or the value of transactions processed through Mastercard’s network. The main types of assessments include:

Domestic Assessments: Fees for transactions within the same country.

Cross-Border Assessments: Higher fees for transactions where the cardholder and merchant are in different countries.

3. Value-Added Services

Mastercard offers a range of additional services that generate revenue, including:

Consulting and Analytics: Providing insights and advisory services to help clients optimize their payment strategies.

Fraud and Security Solutions: Offering tools and services to detect and prevent fraud.

Loyalty and Rewards Programs: Managing and operating loyalty programs for issuers and merchants.

Marketing Services: Assisting clients with marketing campaigns and customer engagement strategies.

Cyber and Intelligence Solutions: Providing cybersecurity and intelligence services to protect transactions and data.

4. Licensing Fees

Mastercard charges fees for the use of its brand and technology. This includes fees for issuing cards under the Mastercard, Maestro, and Cirrus brands.

5. Interchange Fees

While interchange fees are set by Mastercard, they are paid by the merchant’s bank (acquirer) to the cardholder’s bank (issuer). Mastercard does not directly earn from interchange fees but benefits indirectly as higher interchange fees can lead to increased card issuance and usage.

6. Other Revenue Streams

Prepaid Programs: Fees from managing and operating prepaid card programs.

Commercial Payment Solutions: Revenue from products and solutions tailored for business and government clients.

Open Banking and Digital Identity Platforms: Fees from services that facilitate secure and efficient access to banking and identity verification.

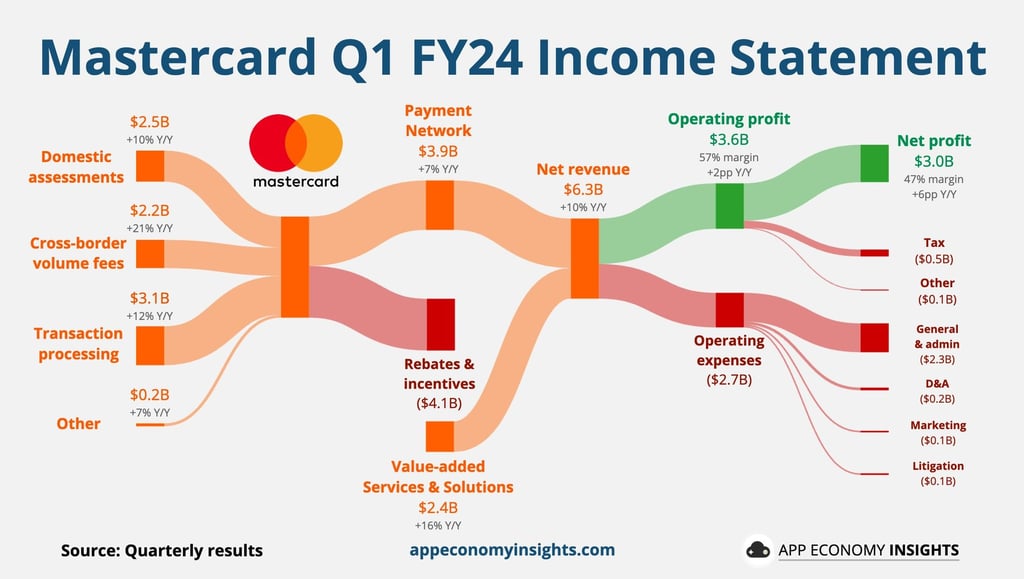

Here is how Mastercard latest income statement looks like:

Fig.4 MA Q1 FY24 result (Source "Appeconomyinsights")

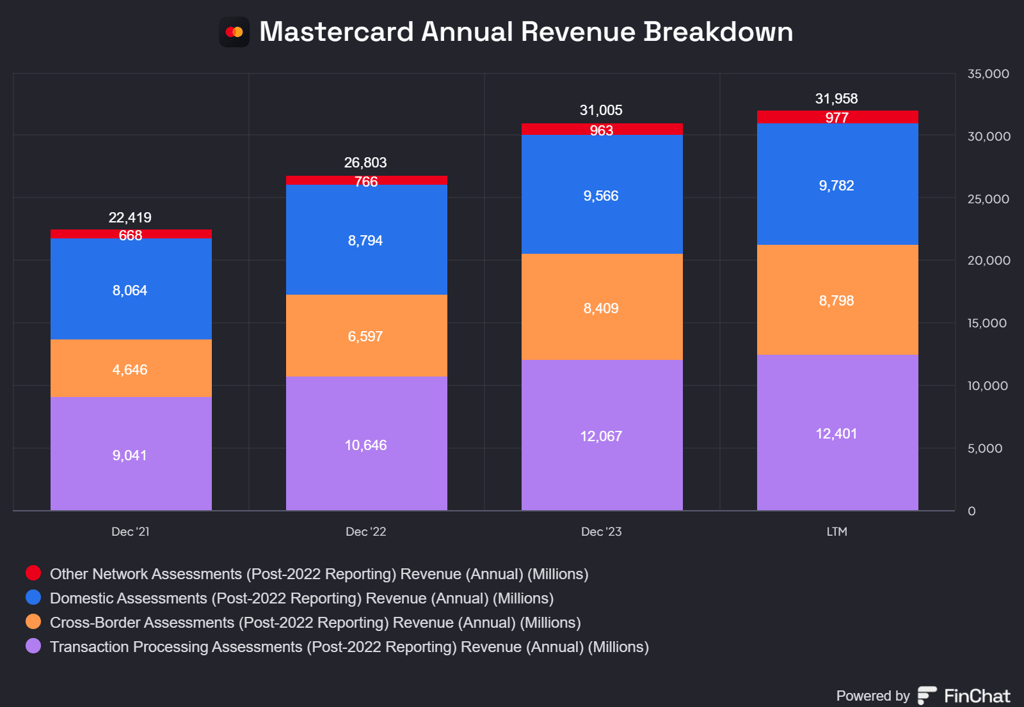

Here is how Mastercard annual revenue looks like for the last 3 years:

Fig.5 MA annual revenue breakdown

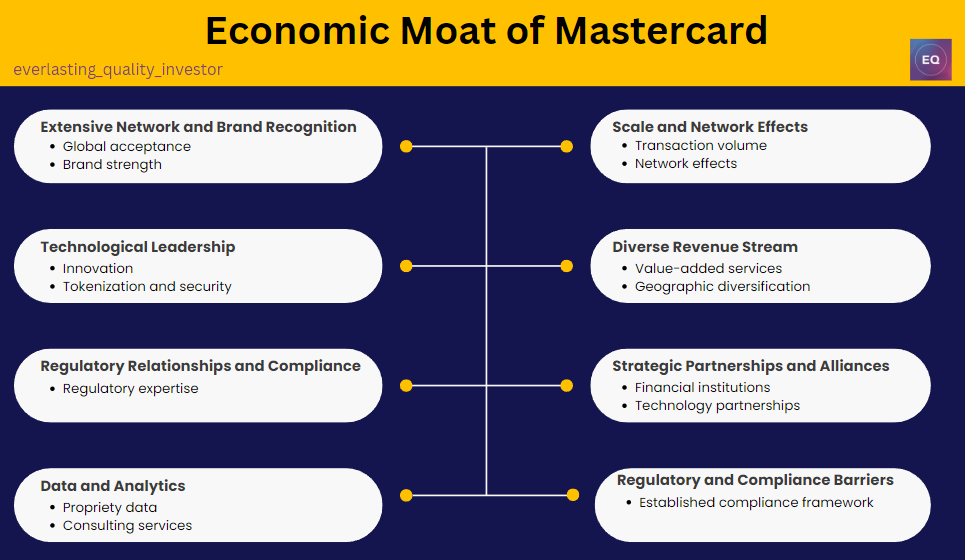

Economic Moat of Mastercard

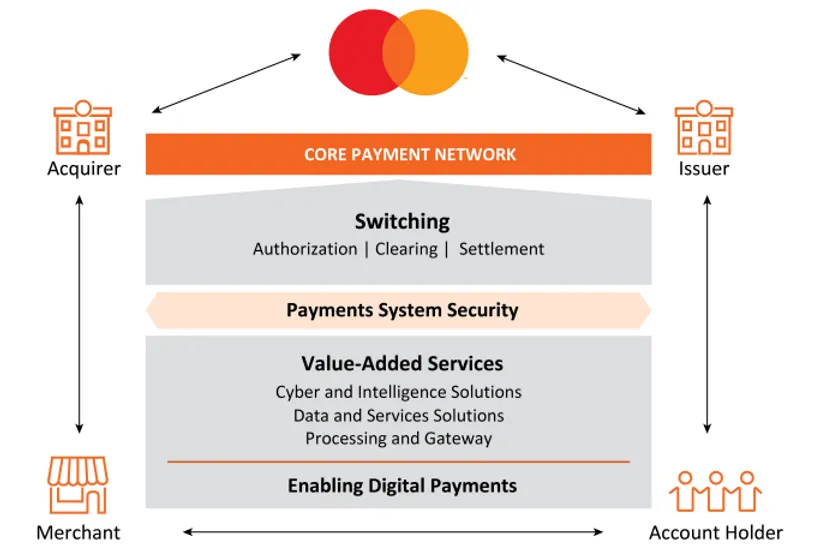

Mastercard's economic moat is built on its extensive network, brand strength, technological leadership, diverse revenue streams, regulatory expertise, strategic partnerships, and data analytics capabilities. These factors collectively create significant barriers to entry for competitors and enable Mastercard to maintain its dominant position in the global payments industry.

Fig 6. Economic Moat of Mastercard

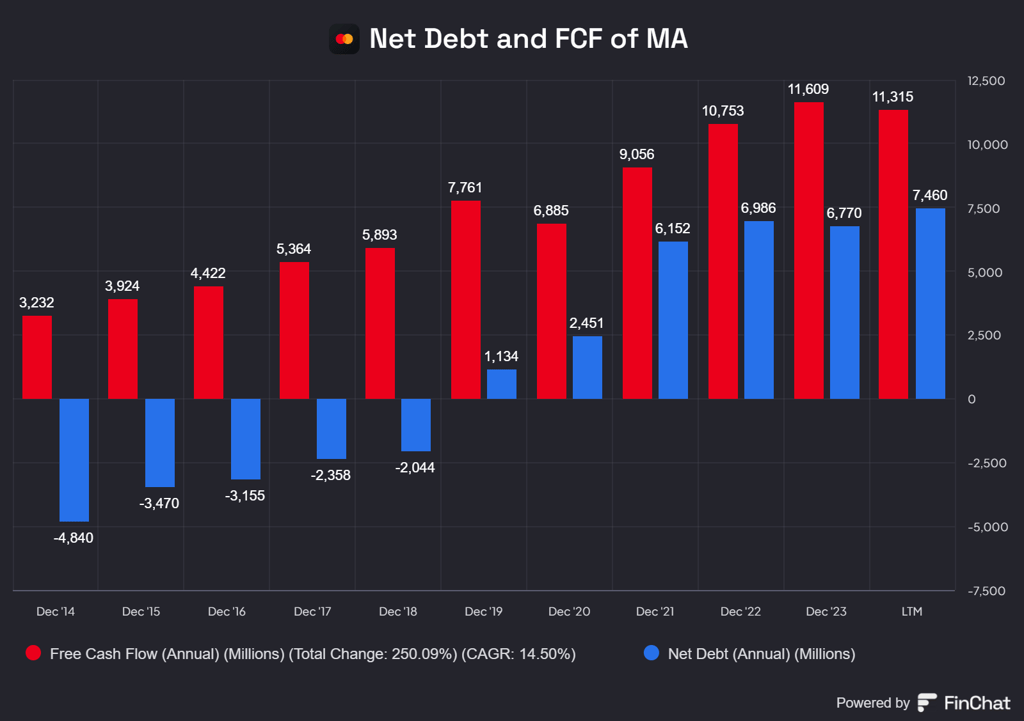

Robust Balance sheet

Mastercard has a healthy and robust balance sheet with a stellar free cash flow. Its net debt is significantly lesser than the free case flow the company generated every year.

Fig 7. MA Balance sheet

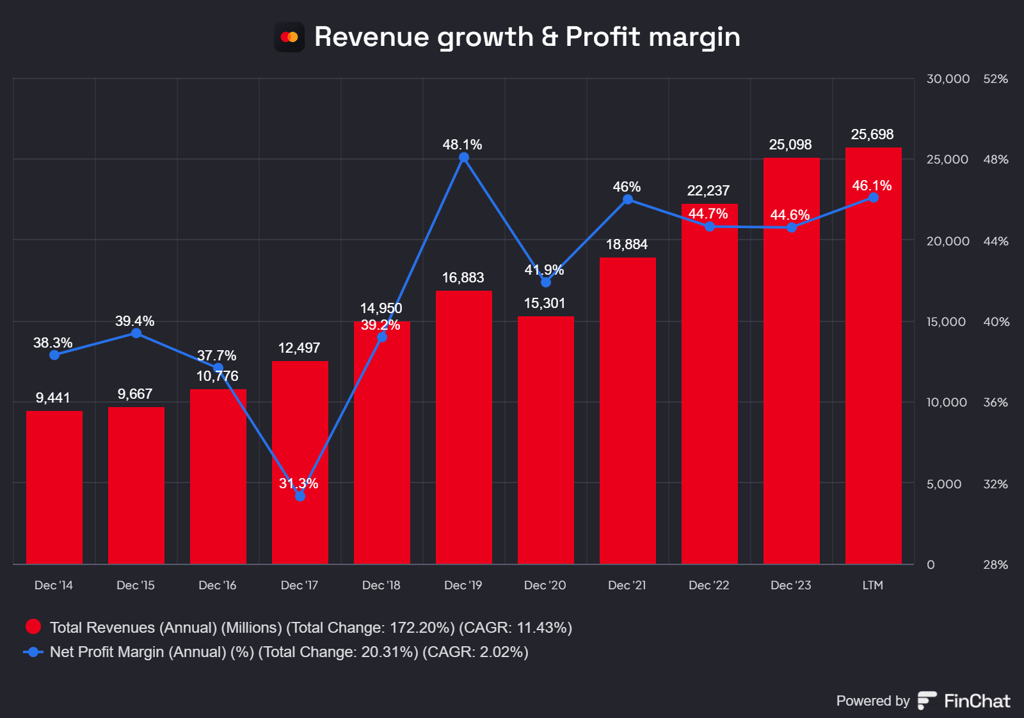

Consistent Revenue growth and Phenomenal Profitability

Mastercard's net profit margin has consistently remained high, reflecting its strong profitability and efficient operations. The most recent net profit margin of 46% for the twelve months ending March 31, 2024, highlights the company's ability to convert a significant portion of its revenue into profit. This strong financial performance is a testament to Mastercard's economic moat and competitive advantages in the global payments industry.

Fig. 8 Revenue growth and profitability

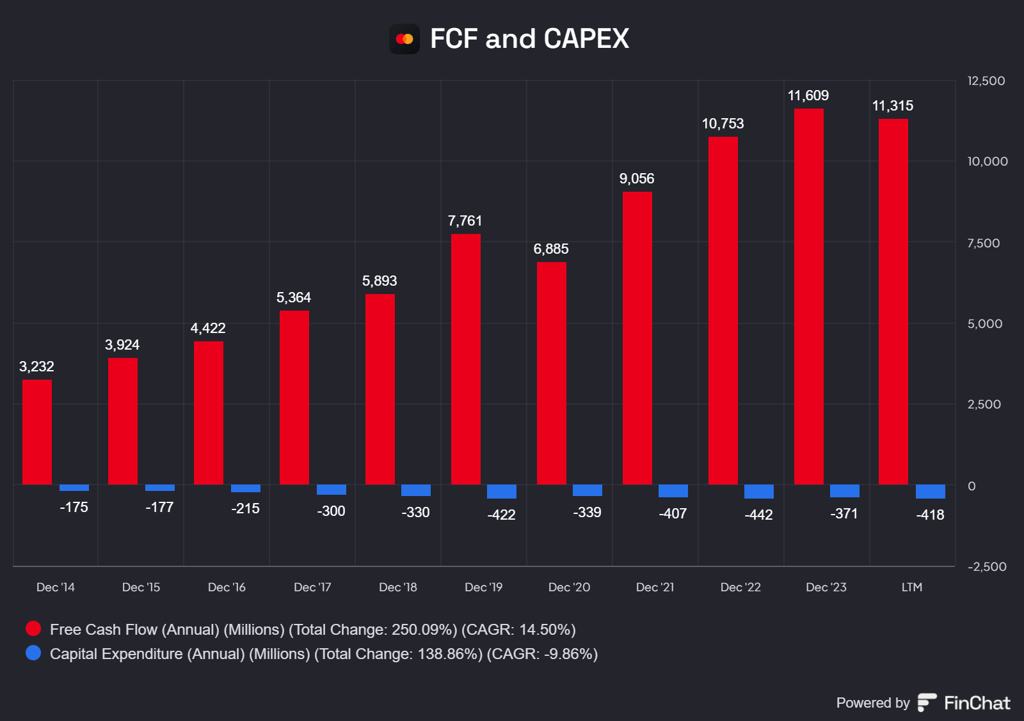

Strong Free Cash Flow with little need of CAPEX

Mastercard's Free Cash Flow has shown significant growth over the years, reflecting the company's strong cash generation capabilities. The most recent FCF for the twelve months ending March 31, 2024, is $11.32 billion, indicating a healthy cash flow position.

On the other hand, Mastercard's Capital Expenditure has been relatively stable, with the most recent CapEx for the twelve months ending March 31, 2024, being -$418 million. This indicates that Mastercard continues to invest in maintaining and upgrading its physical assets, albeit at a controlled and consistent rate.

These metrics highlight Mastercard's ability to generate substantial free cash flow while managing its capital expenditures effectively.

Fig. 9 FCF and CAPEX

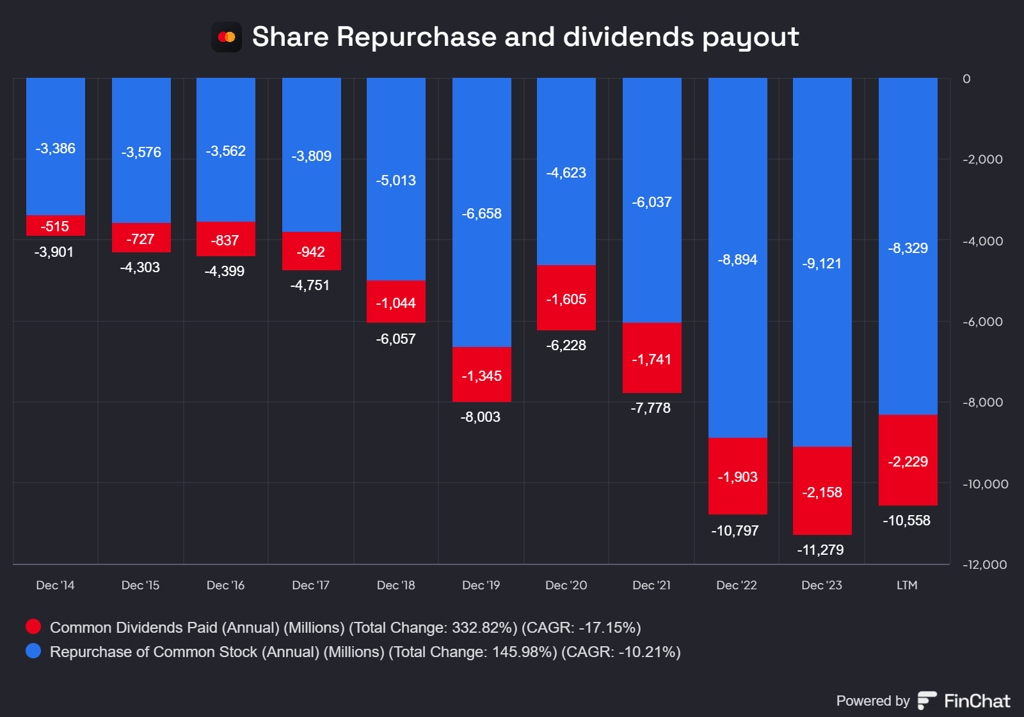

Part of the FCF generated are used to repurchase shares and issued dividends to the shareholder.

*Note: It’s a negative figure because cash is going out of Mastercard to buy back shares and payout dividends.

Fig. 10 Share buyback and dividend payout

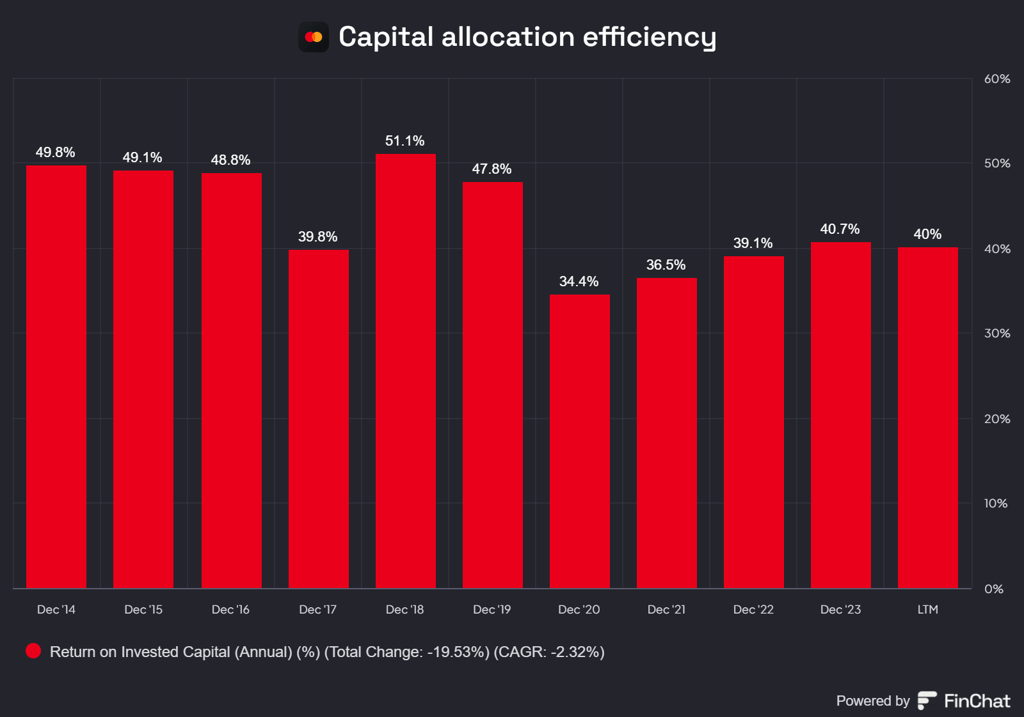

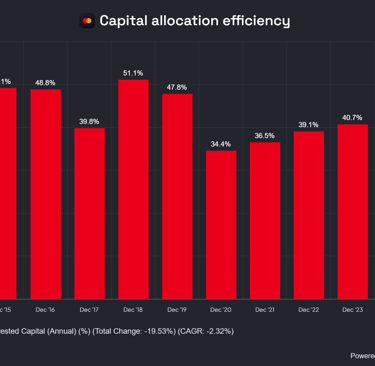

How well Mastercard allocate its capital?

If one wants to access how efficiently a company is using its capital to generate profits, a critical metric called Return on Invested Capital (ROIC) can be used.

A "good" ROIC percentage can vary depending on the industry but well-known investors like Warren buffet and Michael Mauboussin use ROIC 15% and 10% as a general guideline.

ROIC of Mastercard is around 40% and it means they put the money of shareholders to work at very attractive rates of return.

Fig. 11 Return on Invested Capital (ROIC) of MA

Growth and Risk factors of Mastercard

The global payments industry is experiencing significant growth driven by various factors such as the shift from cash to digital payments, increasing e-commerce transactions, spark in travel and expanding financial inclusion initiatives.

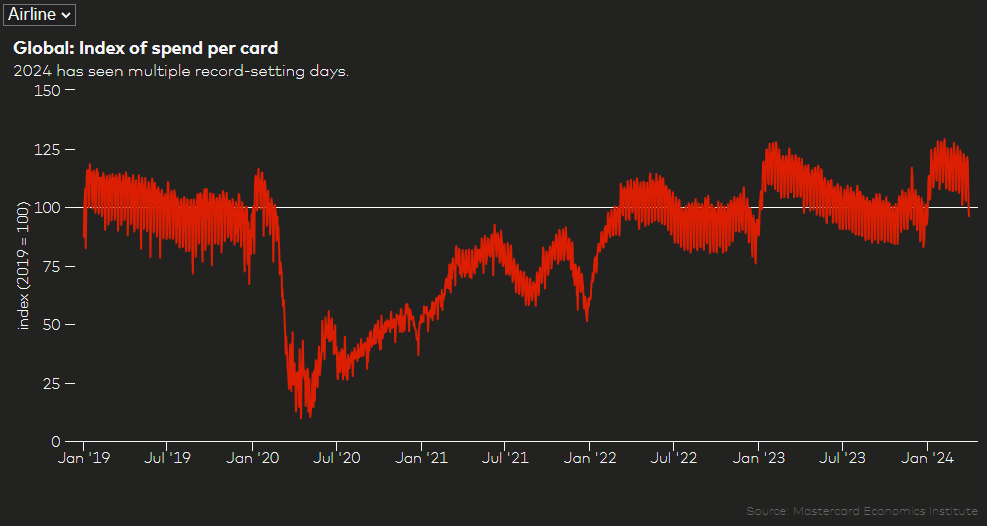

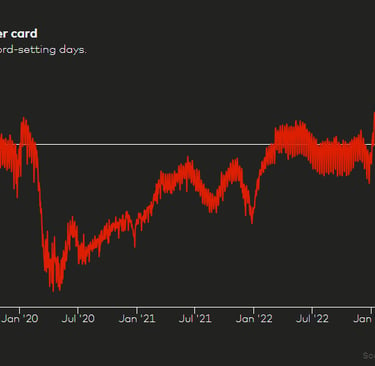

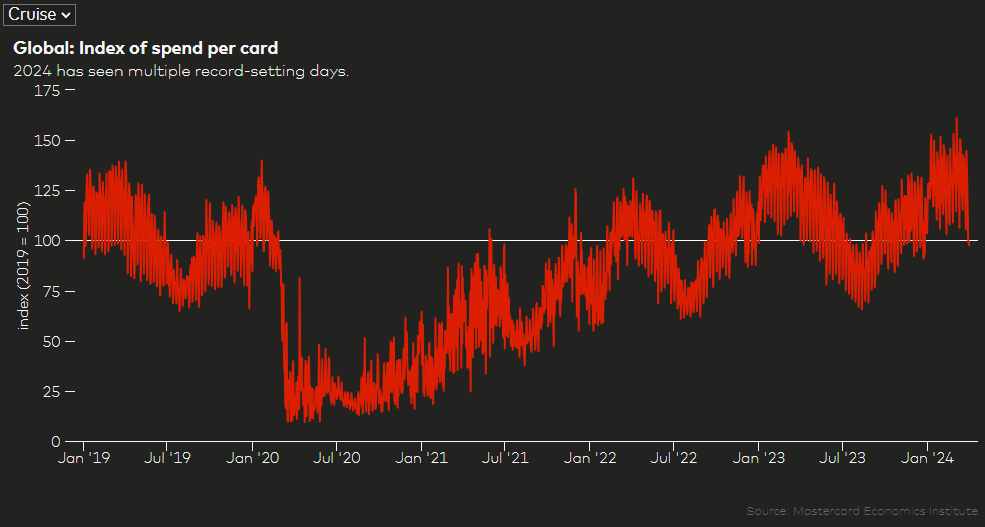

The adoption rate of digital payments and e-commerce transactions was significantly boosted during the world wide pandemic (covid-19) and the adoption is here to stay. 2024 has kicked off with strong growth in the travel industry – in terms of spending but also the number of people traveling. According to Mastercard Economics Institute analysis:

"Globally, nine out of the last 10 all-time record spending days in both cruise and airlines have happened in 2024."

Fig. 12 & 13 Global spending on Airline and Cruise

As one can see from the spending report for airline and cruise, it is safe to say that pre-pandemic records are being broken in travel economy.

Historically, Mastercard has managed to grow its revenue and FCF consistently with

Revenue Growth past 5 years (CAGR): 10.9%

FCF Growth past 5 years (CAGR): 10.6%

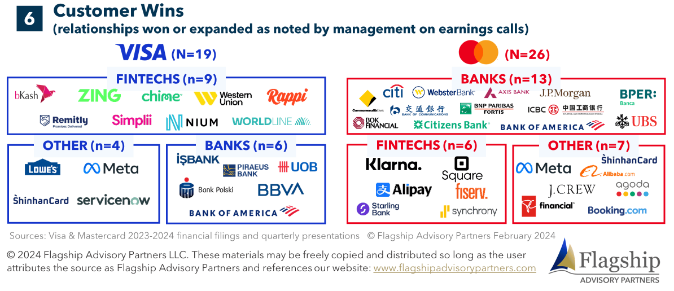

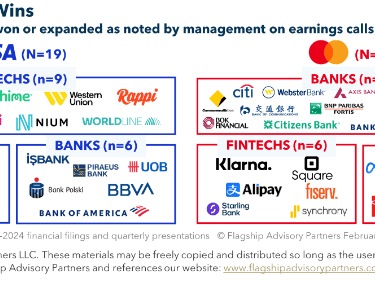

Besides the double digit growth, it has also expanded its relationship with other banks, institutions and big enterprises.

Fig. 14 Expansion of relationship (Source: Flagship advisory partners)

Analyst are expected to see Mastercard revenue and EPS growth as follow:

Exp. Revenue Growth next 2 years (CAGR): 12.3%

Exp. EPS Growth next 2 years (CAGR): 17.0%

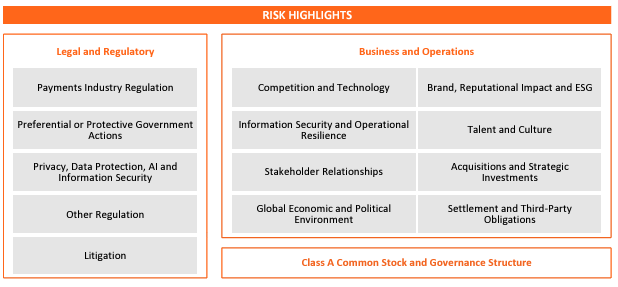

There is no business free from risk and strong business like Mastercard and Visa also has their own risk. Visa and Mastercard are the two most dominant giants in the global payment network in the US. This makes them very susceptible to the regulatory risk if the US and EU government want to reduce their market dominance. Another risk factor to be considered is rapid advancements in technology and changes in payment methods such as crypto or super apps like “WeChat” from China although very unlikely to happen in Western countries.

Fig. 15 Risk Highlights of MA

Valuation of Mastercard

The late “Charlie Munger” once said

"Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you’re not going to make much different than a 6% return—even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive looking price, you’ll end up with one hell of a result."

In a way, I believe we should look for a great business with a fair valuation instead of an okay business with a discounted valuation.

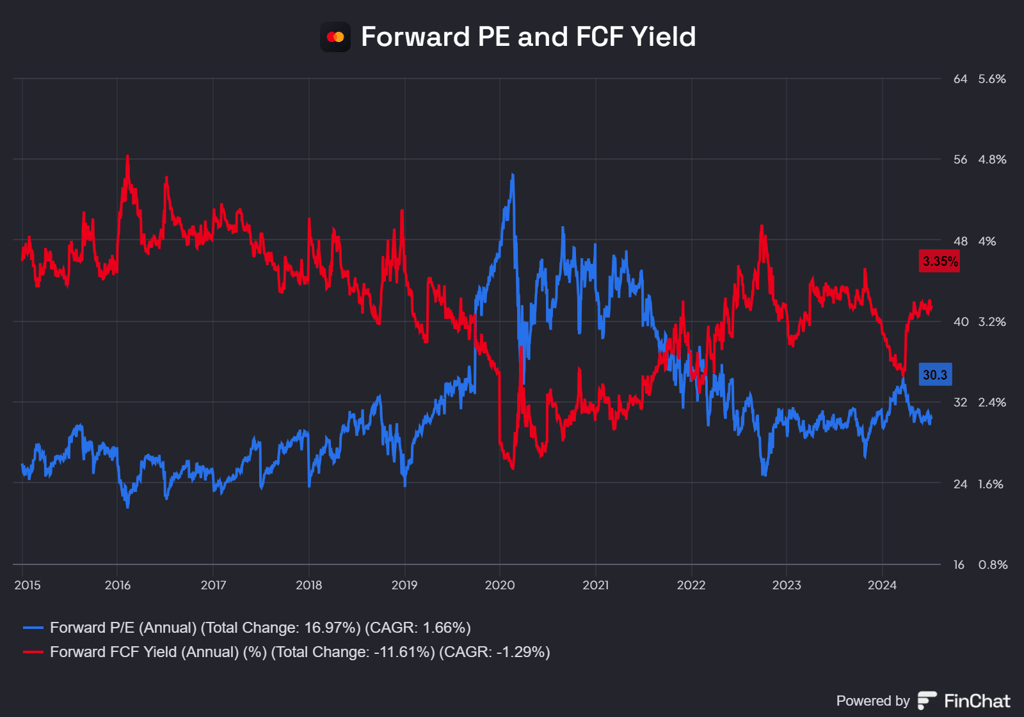

The average historical PE ratio of Mastercard over the last ten years is 36.14x and it currently trades at 30.3x. The FCF Yield of Mastercard is currently at 3.35% which is at the mid spectrum of its range.

Fig. 16 Valuation spectrum of MA

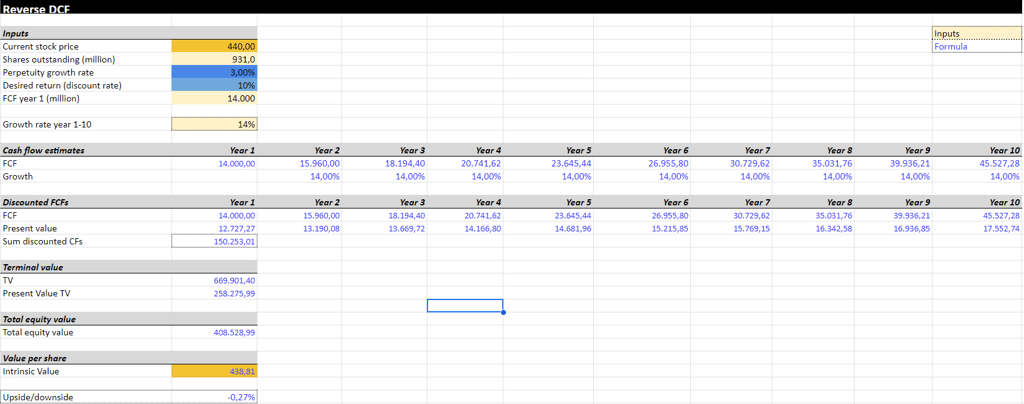

Assuming Mastercard can hit the estimate of 14 billion FCF (consensus from finchat.io) by end of 2024 and I want a 10% return per year, Mastercard has to grow its FCF by 14% per year to meet my assumption.

Fig. 17 Reverse DCF of Mastercard

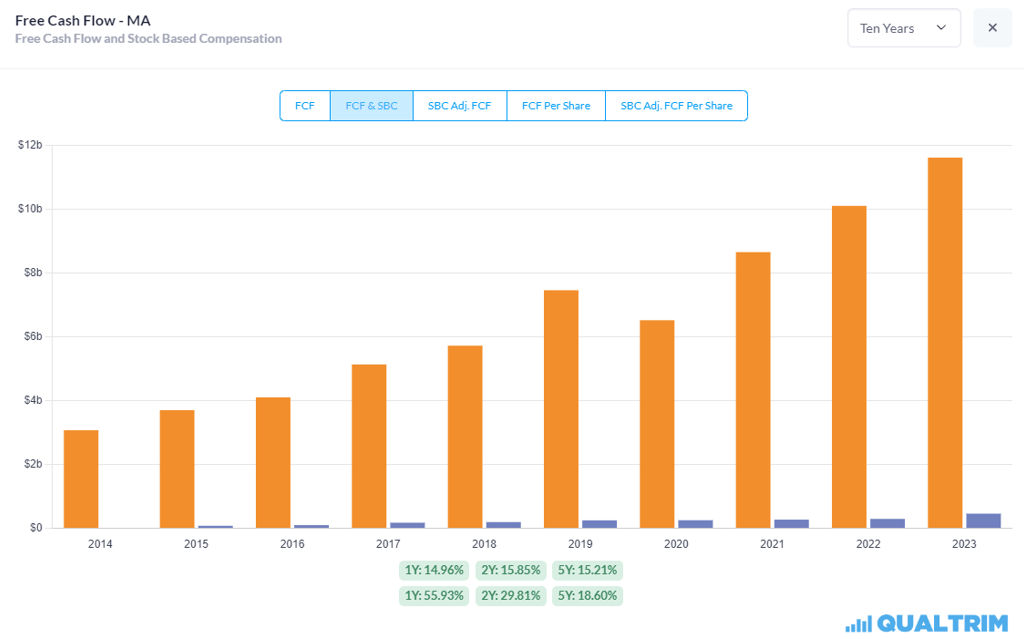

Mastercard doesn’t give excessive stock base compensation and for its FY2023, the SBC is only 3.9% of total FCF generated.

Fig . 18 FCF and SBC of Mastercard

Conclusion

Mastercard is a stellar company with great business in an industry (payment/digital) with secular tailwind. It has pristine balance sheet with admirable revenue growth, great FCF, phenomenal profitability with little to no CAPEX and respectable ROIC. It is a great compounder with ~30% CAGR return since IPO for the shareholders by consistent EPS growth, revenue growth, share buybacks and dividends. Whether it is currently trading at a fair value or not is solely based on individuals and their own preference of assumption.

Disclaimer: This article constitutes my personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, I may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article.

Disclosure – I do hold a position in Mastercard at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).